26 May 2026

Linking Portable Card Readers with Subscription Services Under PCI Guidelines for Local Merchants

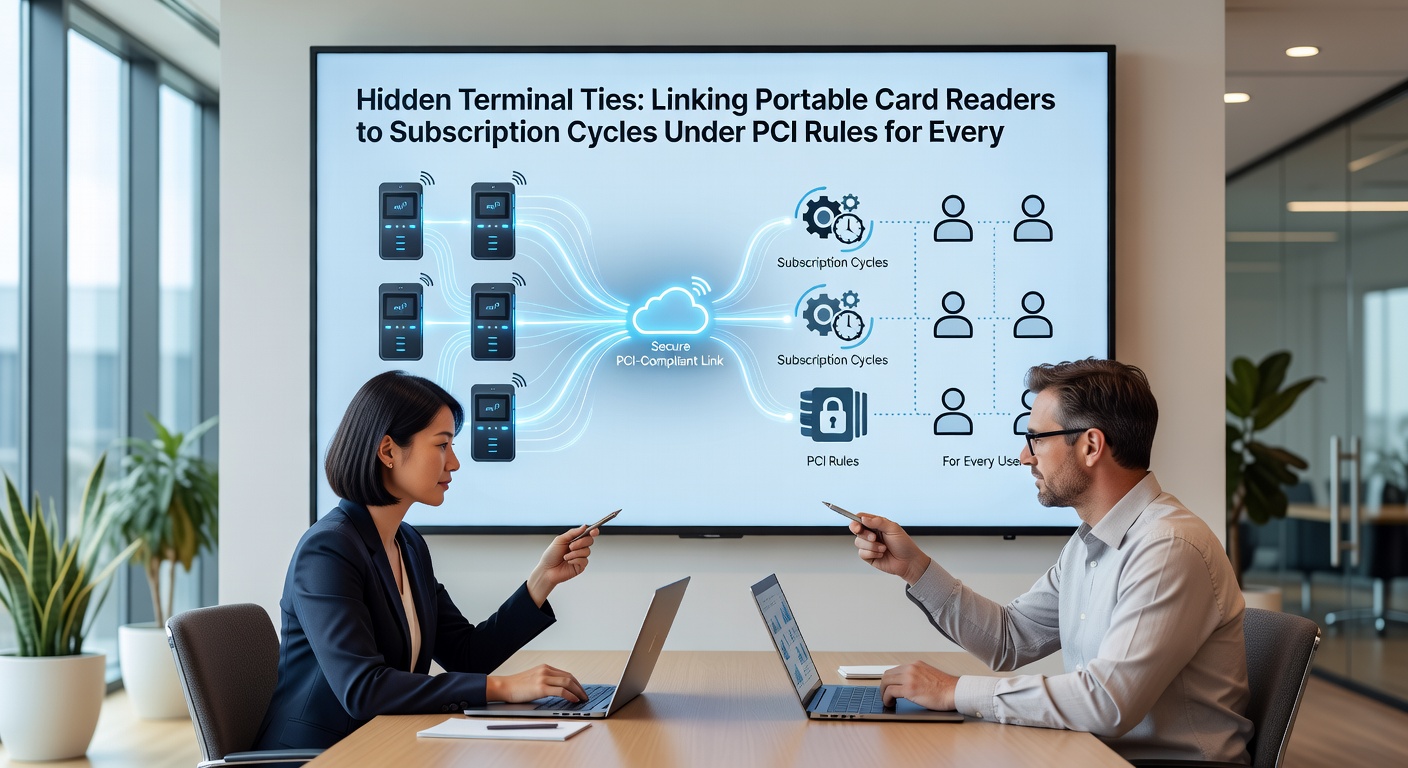

Portable card readers connect directly to subscription billing platforms through secure data channels that meet PCI DSS requirements, and this linkage allows everyday vendors to process recurring payments without maintaining full cardholder data on their devices. Small merchants who operate food trucks, market stalls, or service routes rely on these compact terminals to capture initial authorizations while routing subsequent charges through tokenization systems that shift storage responsibilities to certified processors.

PCI rules specify that portable readers must encrypt card data at the point of interaction, and vendors integrate these devices with subscription software that uses hosted payment fields or direct post methods to avoid retaining sensitive information locally. Data shows that such configurations reduce the scope of compliance audits because the reader itself never stores account numbers beyond the initial transaction window.

Core Technical Connections in Mobile Environments

Bluetooth and NFC-enabled readers transmit encrypted payloads to mobile applications that forward requests to payment gateways, while subscription engines schedule future charges using stored tokens rather than raw card details. Researchers at industry compliance firms have documented that this separation keeps the portable hardware outside the cardholder data environment, which simplifies quarterly self-assessments for vendors handling fewer than 20,000 transactions annually.

Tokenization occurs at the gateway level after the first successful authorization, and the reader receives only a reference identifier for any follow-up actions such as refunds or updates. Observers note that vendors who skip proper token handoff often expand their compliance obligations unnecessarily because residual data fragments remain on the device memory.

Regulatory Requirements Across Regions

PCI DSS version 4.0 outlines specific controls for encryption and access management that apply equally to fixed and portable terminals, and updates scheduled for May 2026 emphasize stronger multi-factor authentication on reader management consoles. Vendors in Canada follow the same baseline while adding provincial privacy overlays, whereas EU merchants align these practices with PSD2 strong customer authentication mandates that affect recurring billing consent flows.

According to documentation from the PCI Security Standards Council, portable devices must undergo annual vulnerability scans when connected to networks that process card data, and subscription platforms must demonstrate that token vaults reside in environments validated at SAQ A-EP or higher levels. This layered approach prevents small operators from bearing the full burden of Level 1 assessments.

Practical Implementation for Routine Operations

Everyday vendors typically pair readers from providers such as Square or SumUp with subscription tools that generate payment links or in-app prompts, and these pairings rely on API calls that transmit only tokenized references after initial setup. Studies from payment research groups indicate that markets adopting mobile POS subscriptions experience fewer chargeback incidents when readers enforce dynamic currency conversion and AVS checks during the first capture.

One documented case involved a fleet of coffee carts that synchronized reader firmware with a cloud billing service, resulting in automated renewal notices sent through the subscription layer while the physical devices remained limited to single-use authorizations. This pattern appears across similar micro-businesses because the architecture isolates each transaction event from long-term data retention.

Security Controls and Audit Preparation

Merchants must maintain logs of reader firmware versions and connection timestamps, and these records feed into annual compliance reports that demonstrate ongoing adherence to PCI requirements. Network segmentation becomes essential when multiple portable units share a single mobile hotspot, because unsegmented traffic can inadvertently pull the entire setup into a broader cardholder data environment.

Training materials from recognized industry bodies emphasize that staff should never manually enter card numbers into subscription portals when a reader is present, since bypassing the device encryption layer violates core PCI principles. Figures from compliance audits reveal that the majority of scope creep incidents trace back to such manual workarounds rather than hardware limitations.

Conclusion

Portable card readers integrate with subscription cycles through tokenization and gateway-hosted processes that satisfy PCI DSS controls while keeping compliance manageable for small-scale operators. Regional adaptations in North America, Europe, and Asia continue to reference the same core standards, and forthcoming refinements in 2026 will further clarify authentication expectations for recurring authorization flows. Vendors who align device configurations with these established linkages maintain operational flexibility without expanding audit requirements.